Critical Changes to CGT

From 6 April 2020, anyone making a taxable gain from the sale of UK residential property will have to pay the Capital Gains Tax (CGT) owed within 60 days of the completion date.

CGT was previously paid as part of annual self-assessment returns. This therefore means a significant change. A payment that could have been made between 10 and 22 months after the date of sale is now due almost immediately. There are also changes to letting tax reliefs and final period exemptions outlined in our full factsheet.

Common Questions regarding the 60-day payment window

- Are there any applicable tax reliefs that can reduce the tax due?

- How will the tax payment affect my annual self-assessment return?

- Can I still offset capital losses against the gain?

Other changes in summary:

- Letting relief rules tightened.

This tax relief on previous main residences will now be limited to those who shared occupancy with their tenant. Previously this relief may have exempted £40,000 of the gain (so £80,000 for co-owners). - Final period exemption reduced.

If a property was ever a main residence, in most cases the last 18 months of ownership qualify for private residence relief and are exempt from tax. This will now be limited to 9 months.

General Advice for Property Investors

As a landlord or property investor you must consider tax liabilities at the various phases of owning and renting a property, from purchasing, letting and on sale.

Recent Articles

- Short-term let owners to face new planning permission requirements

- Investing in property: The tax implications

- Landlords should bring UK tax affairs up to date before Renters Reform Bill is enforced in law

- Sharpest house price fall in two years

- Autumn Statement: Slashing CGT huge blow to landlords

- Autumn Statement: Stamp duty cut will end in 2025

- Councils given the flexibility to increase council tax and social rents capped at 7%

- Landlords targeted over undeclared income from residential property

- Time to rethink your property portfolio? What you need to consider

- The energy price cap and what to expect from your energy bills

Free Resources

- Take advantage of Land Remediation Relief

Find out if your Companies may be eligible for up to 50 per cent tax relief.

- CGT Planning for Residential Property

In April 2020, three changes may increase the capital gains tax you need to pay when you sell a residential property. Make sure you are aware and take them into account.

- Property as an investment

With low interest rates, property remains attractive.

- Furnished holiday lettings

Your reference to the pros and cons of letting furnished holiday accommodation.

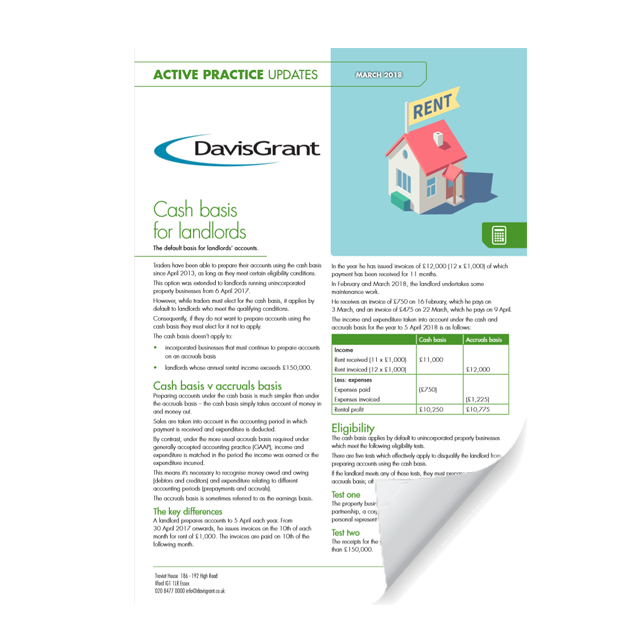

- Cash basis for landlords

A summary of the default basis for unincorporated landlord's accounts